Withdrawal of VAT

In summary, the following services are now subject to the exemptions from value added tax (VAT).

The amendments relate in particular to:

• travel services resold by domestic and foreign travel agencies

• active participation in cultural events

• the services of coordinated care for medical treatments

• providing infrastructure to affiliated doctors in outpatient clinics and day clinics

• the care and housekeeping services provided by private Spitex

• the provision of personnel by all non-profit organizations

Simplified annual billing for small businesses (Annual billing)

From January 1, 2025, companies with an annual turnover of no more than CHF 5,005,000 can file an annual VAT return upon request.

In order to benefit from the annual VAT declaration, previous and future VAT returns must be submitted and paid in due time.

The application to switch to annual reporting can be submitted via the ePortal from January 2025. To submit an annual report for 2025, the application must be submitted by February 28, 2025. New taxpayers have 60 days after receipt of their sales tax identification number to apply for the annual report via the ePortal.

There is no change in the content of the annual report, meaning that corrections, annual votes or deadline extensions are possible. The annual return must be submitted and paid by the end of February of the following year.

The annual report is subject to an obligation to pay advance payments. If the effective and lump sum method is used, three advance payments must be made, which are due on May 30, August 30 and November 30. With the net tax rate method, payment is due by August 30.

Interest is charged on late payments or advance payments that are insufficient in relation to the VAT actually owed. In our opinion, this “simplification” is not an improvement in many cases, as the costs of filing quarterly VAT returns will continue to be required.

Net tax rate method (Net tax rate method / Flat tax rate method)

More than 2 net tax rates are now possible. The 10% rule remains decisive, i.e. a new net tax rate must be applied if the share of revenue from the respective activity exceeds 10% of the total taxable turnover.

When switching from the effective settlement method to the net tax rate method (and vice versa), the value of the brought in warehouse must now be taxed, or the input tax claimed on it must be corrected (analogous to deposit tax, or as a self-consumption adjustment).

Some balance and flat tax rates were reviewed and redefined by the FTA.

Special procedures relating to exports (Form 1050), the recording of fictitious input tax (Form 1055) and margin taxation (Form 1056) were abolished.

Activities that require an additional net tax rate can be applied for and reported directly in the VAT return. The FTA carries out an examination and then issues the permit.

Are you planning to switch to a different billing method on January 1, 2025?

The request to change the method must be submitted before February 28, 2025. We will be happy to help you assess whether a change in billing method is beneficial for you and assist you with the application process.

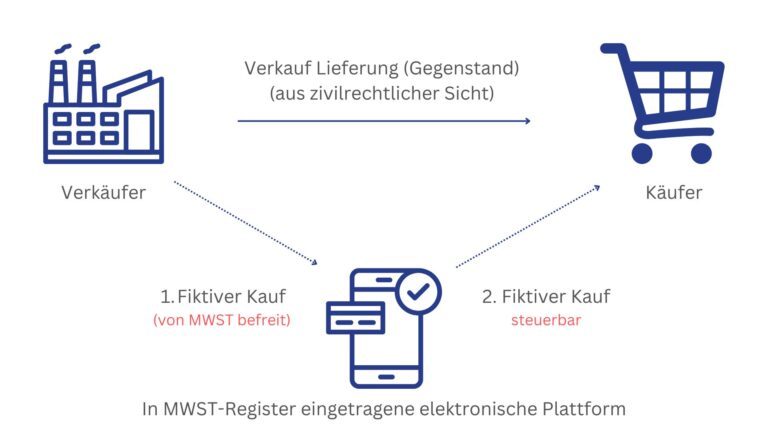

platform taxation (Electronic platforms)

From January 1, 2025, VAT on sales via electronic platforms subject to VAT will be attributed directly to the platform. This must collect the tax, process it correctly and declare it to the FTA. Sellers should check whether the platform is registered in Switzerland and acts in accordance with the rules, as they may be subject to subsidiary liability for VAT.

Platform operators as service providers

When a platform brings a seller and buyer together, the platform operator is considered a service provider to the buyer. This results in two deliveries: one between seller and platform operator (tax-exempt) and one between platform operator and buyer.

Tax exemption and declaration

The first delivery is tax-exempt and must be declared under section 220 in the VAT statement. It is possible to voluntarily tax this delivery.

Billing methods

Companies that sell via platforms can switch to the effective billing method and choose an annual billing method under certain conditions.

Place of delivery

In the case of imports, the place of first delivery is abroad and must be declared under section 221.

invoicing

Sellers must state on invoices that this is a transaction in accordance with Art. 20a VAT Act and name the platform operator.

Duty to provide information

Platform operators only have to provide information upon request from the FTA, not automatically.

Voting on imports

Coordination between declared sales and import tax is not required for the time being.

Subsidies under the revised VAT Act (subsidies)

The new VAT Act provides for the following when allocating subsidies (Article 18 (3) of the VAT Act):

_ “If a community expressly refers to the recipient as a subsidy or as another public service contribution, these funds shall be considered a subsidy or other public service contribution within the meaning of paragraph 2 letter a.” _

January 2025 is therefore decisive for value added tax as to whether the community expressly describes the cash flow as a subsidy.

If this is the case, for VAT purposes, it is a subsidy that represents an untaxable cash flow.

Subsidies are therefore not taxable, but can result in input tax deduction reductions for the recipient (cf.

The accounts of the community are audited by the financial control, the auditor or the financial commission.

The FTA's draft practice provides that financial resources may not only be described as a “subsidy”, but also as “financial assistance” or “government contribution,” depending on applicable legislation. This is to ensure that the new regulation can be applied.

Designation as a subsidy must be made explicitly by the end of the finalization period at the latest

The partially revised VAT Act regulates that the designation as a subsidy must be made “expressly” and “vis-à-vis the recipient.” The name must therefore be brought to the attention of the recipient individually.

Ideally, it should be described as a subsidy at the latest until the corresponding amount has been paid out. However, the Value Added Tax Ordinance (MWSTV) also provides in Article 29 (2) that the designation as a subsidy is permitted even until the end of the finalization period of the tax period (Article 72 (1) of the VAT Act) in which the payment is made.

The paying community must prove to the FTA that a payment was described as a subsidy. The FTA recommends that this be documented in writing. If a payment is not described as a subsidy, that does not automatically mean that it is considered a taxable payment. The FTA can continue to check how the cash flow is to be qualified.

Online obligation (Online VAT obligation)

From January 1, 2025, all companies subject to VAT must settle VAT online via ePortal. The settlement form can no longer be ordered on paper.

Further information on the partial revision of the VAT Act and the VAT Ordinance can be found here:

VAT Act with amendments from 2025 (PDF, 1 MB, 19.12.2023)

VAT regulation with amendments from 2025 (PDF, 657 kB, 11.10.2024)

Your MKY Treuhandpartner GmbH

Disclaimer: The content of this blog post is for informational purposes only and does not constitute professional advice.

Each individual case should be reviewed individually and we recommend that you seek professional advice for specific questions.